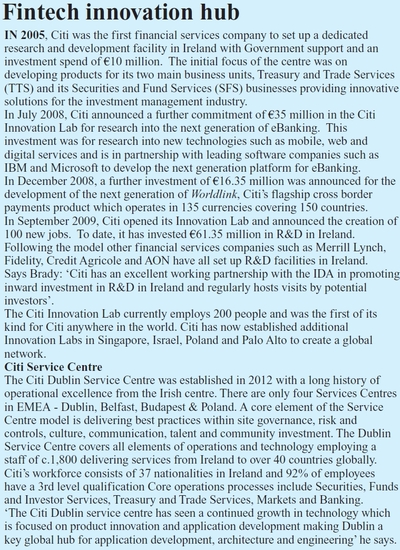

| Citi - Ireland’s international banking success, a template for cross border banking in an era of European banking union |

Back |

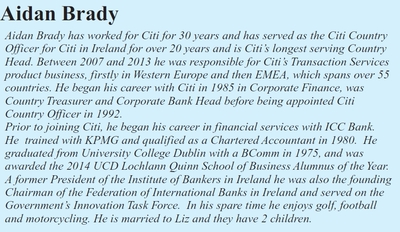

| Finance Dublin interviews Aidan Brady, country head of Citi in Ireland, and chief executive officer of Citibank Europe plc which is the headquarters of Citi's Central European branch network, on the story of the remarkable business that Citi has built in Ireland and its implications for the international banking sector in Ireland in the imminent era of European banking union. |

The storms that have buffeted banking globally, in the eurozone, and in Ireland have affected the international banking sector in the IFSC more than perhaps any other sector, yet, Citi, employing over 2,500 people, managed locally by Aidan Brady, has continued to develop and expand its Irish regulated bank, Citibank Europe plc, and the creation of Citi’s first ever Innovation Lab. This, in the midst of the perfect storm of the eurozone banking crisis breaking around the economy of his native country, in his native city. | | Aidan Brady: a different form of financial services today |

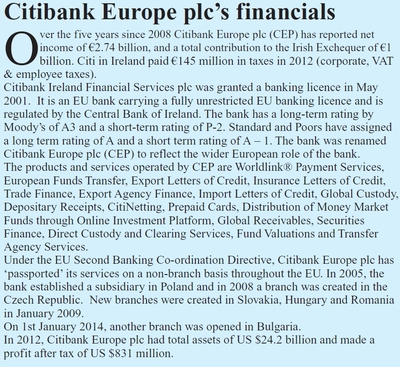

The judgement calls of Citi in building their business model in Ireland have proven prescient. It is almost as if the bank, Brady, and its Irish management anticipated this outcome when the crisis broke in 2007-2008. Starting in 2008, Citibank Europe plc began to open branches in Central Europe and over the five years since has reported profits of €2.74 billion, and a total contribution to the Irish Exchequer of €1 billion.

Today, it comprises 25 to 30 different business units. 'If you were to compare any multinational, there are three things you would like to see: jobs, because that's key; you'd like to see a contribution in tax, and you would like to see an intellectual capital component. If you add those three as an index, we are in the top 3 to 5 multinationals in Ireland”.

Looking forward, he is surveying a scenario that seems all positive: the European Union scenario, with the proposed establishment of the European Banking union plays right into the hands of Citi's plans, because a single European regulator sets the scene for a single banking market served by an institution headquartered in Ireland, while the Irish businesses' two other planks - fintech, and operational risk governance offer huge opportunities in the decade ahead.

On fintech, he says “technology in financial services has to be a massive opportunity – and I am not talking about a 100 jobs here and a 100 there – I'm talking about at least 5,000 jobs.

“If you really want to push the boat out, the connectivity is massive in the marrying of financial services with technology – and Ireland has a reputation in both.”

“If you look at what we in Citi have done in the space of three or four years, we now have 400 technology people and you're talking about engineers, solution architects, project managers, software developers, really in the high end of technology. We are now probably one of the biggest software companies in Ireland.”

The third plank is Governance, another big theme for the IFSC, he says. “With the big legal vehicles that we have there is a bucket for operational risk, which covers different risk than market risk and credit risk - more technology and operations risk.

“We make trillions of payments per year, per week, of all types, that are subject to various kinds of risk whether its operational risk, financial risk, or technology going down, for example. It's an area of interest that we have and an area of interest that the Regulators have – but it is probably the least researched and developed area of risk, and it is such a broad area.”

“Ireland could become a hub for a lot of that work. What you could see potentially happening is the amount of regulation, intensity around anti money laundering, sanction screening, whatever, - operational risk in general. We actually provide anti money laundering support to the relationship people around the world - providing information about clients is based out of here. So my point is that Ireland could become a centre for employing people to do operational risk type tasks”.

“They are the broad themes of what we're going to do: our legal vehicle will grow; our technology will grow, and our concentration on risk and Ireland becoming a utility for risk management will grow”.

During the great deleverage of banking, and international banking, including the international banking business in the IFSC there has, since 2008, been a scaling back of balance sheets, including the closure of a significant number of international banking branches in Ireland. In this light, we ask, how does Ireland appear as a future banking hub, and as a host for Citi's plans, given the view that headquarters banking is not for small countries?

“Our evolution since 2008 was very significant for the future one could say, because we are one of the few banks left in Ireland (probably the only one) that has branches outside of the country. So because of our capital position and our governance structure, and the types of products we have, attracting Central Europe into our legal vehicle, Citibank Europe plc was a good fit. So it works: Hungary, Romania, Slovakia, Czech Republic, Poland and recently, Bulgaria - that all has worked extremely well. This pan European business is regulated out of Ireland. Hungary, for example, would have a customer business like ours, here in Ireland, serving the top end of large multinationals, it has an SME business and it has a consumer business, quite extensive entities. The fact that this has been implemented and has proven to be successful from a corporate governance point of view, bodes well from an Ireland prospective and for having Ireland as a headquarters location for banking in the EU.

“You might have had worries about Ireland as a location in 2009-2010 but the fact that Ireland has come out of its difficulties in a very strong way is hugely positive for sentiment towards Ireland now. We've taken it on the chin, we have moved on, we've learned the lessons, hopefully, from that and are more realistic about our position in the world, we've got ourselves firmly footed.

“Some people have quoted a comment to me about a year ago from the Governor of the Central Bank to the effect that having a headquartered bank out of Ireland was not particularly authentic”, he continues. “I do not believe that he was referring to us. I think he was referring to Irish banks going back to trying to be international banks - I hope he wasn't talking about international banks having a base here. I suspect not.”

“Going back to that earlier point, it's probably changed a little bit, the authenticity of it depends on what business you're doing, depends on the size, if you're a large enough size you become part of the overall market.

“I think the point is in danger of being lost, but Ireland should not be shying away from doing more business out of Ireland. That would be a mistake and I hope that, I suspect that, the Central Bank would be behind that.

“We should be doing more and more business out of Ireland and encouraging companies to come here - be they financial services or any other type. I wouldn't make too much of that but I wouldn't like Ireland to get cold feet about its position in the world because we've made mistakes. But hopefully we've learned from those mistakes.

So to think that a European bank would move its headquarters to Ireland is probably unrealistic but overseas banks that are outside the region that want to be in Europe might find Ireland to be a good location to have a base. Citi is an example of that. Having a HQ for Central Europe through Ireland has worked extremely well. You don't do that without thinking it through - it's the knowledge base of understanding the products, the line of business you are doing.

“So for example tomorrow it would not be particularly plausible for us to start a big markets business in Ireland as we don't have the skills base. We don't have the DNA. We did have it years ago - I was a treasurer, we were a small team but I'm sure at the start of the IFSC Dermot Desmond had the idea of traders placed here but that just didn't work.

So it's a different form of financial services today - transactions services will work, a certain amount of lending will work, banking, obviously, consumer, to an extent, would work although that's not really cross border, - you have to be in the country to do consumer banking. The whole technology development side and lots of areas will work here and other areas won't. I think we're more realistic about that now.

“All of that could be regulated out of here in the European banking union - what's changing that slightly, size wise is the single supervisory body. You get to a certain size you go into the single supervisory - under the rules of the future, that makes it more plausible that you could be located anywhere across Europe and you've got standardized regulation which I think would be great - making it easier for people to be in this country or the next country. One regulator and one set of standards suits us perfectly from that point of view.”

All of our Central European units would be within the ECB framework – that works and that makes sense. So a single market and having a strong regulator in Ireland - even if you're based here and you are under the SSM (Single Supervisory Mechanism) you'll still be regulated to a large extent out of here, so having a strong regulator, which we do have, is good. Developing a single regulator rather than an independent regulator is good for this jurisdiction. It also bodes well for developing the quality & skill of regulation in Dame Street, which would make, incidentally, this jurisdiction the largest English speaking unit within the eurozone.

This governance work will mesh with the fintech future that Citi has rolled out in its business model, ever since it set up the Citi Innovation Lab, in Dublin, which became a prototype for R&D units in the IFSC as part of the IDA's programme, and indeed within Citi globally.

“On the tech side,” he says ‘the number of interesting start up financial services type tech companies that are popping up in Ireland is most extraordinary.’

“It's a very interesting area which we should be putting a lot of attention to. The IDA should be spending a lot of time attracting this type of industry to Ireland. Obviously there's a limited skills base but over time a company like ours, in this area, is going to become more and more digital. I'm a traditional treasury banker but the people that will be running the businesses that we run, in ten years time will be in technology with huge technology backgrounds. That's where the game is.

“Banking in the future won't be only about lending people money it will be about trade - facilitating customers to do their business. That's a mistake that a lot of companies make when they are targeting financial services - they think it's just about credit.”

The business has come a long way, since he, in the 1980s, along with Tony Golden, a one time multiple winner of the Finance Magazine/Finance Dublin/IACT Dealer of the Year Awards and other illustrious members of the Irish corporate treasury industry ran a business serving large Irish corporates. Looking back, what were the key points, we ask him, along the way.

“For example, back in 2001, when Finance Dublin reported on the establishment of CIFS (now Citibank Europe Plc), you expressed satisfaction that Citi had decided to locate a centre of excellence for a business model that is increasingly recognised as a strong growth path for banking globally?

“Looking back”, he says “you would have to say that that particular initiative to set up a bank has been more successful than we could have dreamt of in our wildest dreams, to be honest. But looking back further than that, to the early days of the IFSC, what we were trying to do was, responding to the obvious, Ireland being a cost centre, to build a big operation of the scale of the service centre, because Irish costs were relatively low, and there was a big supply of talent.

“It became increasingly obvious as we went through the 1990s and the boom in the IFSC, that cost wasn't going to be the driving factor. So we decided that moving to being a profit centre was probably the way to go, moving up the value chain of skills, building products, and developing products.

It was a nice idea anyway, and we implemented it with one person, myself, and one employee. It was built around a simple idea of doing corporate governance, would you believe, for lots of entities that we had around. We thought we would move off treasury centres and go on into corporate governance.”

Was it an example of intrapreneurship, and would you describe that as an easy process?, we ask.

“These things happen because they're sort of obvious, maybe not as obvious to other people, but it wasn't an easy thing to get done I have to tell you. Citi didn't want to create more legal vehicles, it was closing down legal vehicles in fact. So there was an element of, being a little bit under the radar within Citi and having to set up our vehicles for really good reasons.

“There were lots of ideas, but from a pure Ireland point of view it was to build that business model, it was to move from having a good customer business in Ireland, but with limited resources, to build off what we have been lucky enough to create in the 1990s - the Service Centre. The question was what do you do next? the answer - you use the IFSC to develop products to sell worldwide.

“So I concluded, you set up the bank as a cover for all those other things, so the real essence of it became attracting products into Ireland and to convince management elsewhere that Ireland was a good place to put our payments products, trade products, full service products. We found that operations may be one thing but product management excellence is the fundamental key to convince people that you have the capacity to do this. It was, and is, a slow process.

But today, 2,500 jobs, and over €1 billion of tax revenues later, a prototype exists that seems perfectly poised to carry on a remarkable tale of Irish international financial services success. |

|

|

| |

|